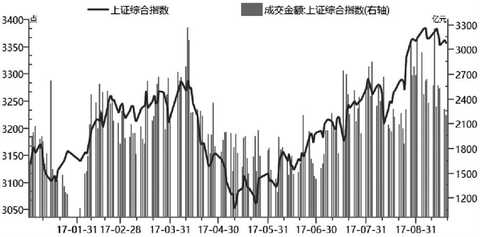

It is expected that the pattern of weak IH and strong IC will continue Since entering September, the market has entered a period of consolidation after the rise. After a high level of consolidation for 14 consecutive trading days, the market chose to step back and the market volume also shrank sharply, indicating that the short-selling momentum was not strong. Market hotspots switch back and forth between the plates, the overall is more scattered and the continuity is not strong. In terms of style, the market style gradually switched from partial cyclical stocks to large-scale consumption sectors such as liquor, home appliances, food and beverage, and some institutional funds that withdrew from the cyclical stocks had a tendency to switch to the consumer sector. Investors began to turn their attention back to low. Valuation and performance on the white horse. Pre-holiday market capital fabrics will be tight After entering this week, the central bank put a lot of liquidity into the market through reverse repurchase operations in the open market, but the effect has not changed the short-term market funds. The most intuitive performance is that the interbank pledge repo rate has risen most, especially the demand for cross-month varieties is strong, and the short-term and medium-term Shibor and various government bond repo rates have also risen. We believe that this is mainly due to factors such as monthly tax payment, quarterly MPA assessment and “11†long vacation provision. From a historical point of view, after entering the end of September, the organization will usher in a crucial period of preparation for the inter-season and long-term provision, and the liquidity demand will show an upward trend. The contradiction between liquidity supply and demand will intensify in a short period of time, thus triggering liquidity tightening. . This week is the global "super central bank week", the three major central banks of the United States, Japan, and Europe will hold interest rate meetings this week. Among them, the Fed’s two-day monetary policy meeting will be held on Tuesday and Wednesday, and the interest rate decision will be announced at 2 am Beijing time on Thursday. The market expects that the Fed is likely to officially announce the reduction of the balance sheet, the start-up time and operational details of the “shrink-down†plan, after this interest rate meeting. If the Fed announces the start of “shrinking†after the meeting, as expected by the market, the impact on short-term market liquidity cannot be ignored. Market style begins to show signs of switching Following the decline in domestic macroeconomic data in July, last August's macroeconomic data released by the Bureau of Statistics was lower than market expectations. Industrial indicators such as industry, investment, consumption, import and export fell for two consecutive months, leading to the next market. There are large pessimistic expectations in the macroeconomic trend of the stage. The lower-than-expected economic data directly triggered a general fall in the prices of commodity futures and cyclical stocks. Recently, the spot price of industrial products and metals in South China has also dropped significantly from a high level. In addition to the market's expectation of the economic downturn in the fourth quarter, the limited production of heating seasons has also become a new variable in the fall of cyclical stocks. As the short-term stock index enters a high consolidation period, the economic data of July and August for two consecutive months is pessimistic. The market has a big divergence in the future trend of the cyclical stocks, and funds are beginning to return to the large consumer sector. Since last week, we have found that the strong consumption of liquor, home appliances, food and beverage, automobiles and other large consumer sectors in the first half of the year, after a few months of brief corrections, began to receive funding attention and showed signs of starting. From the perspective of configuration, we believe that in the context of the current index's large probability of maintaining range oscillations, the market style is expected to return to the defensive sector with low valuation and strong performance support. In the short term, liquor, real estate, construction, home appliances, food and beverage, etc. Value blue chips may be stronger again. The pattern of strong IH weak IC will continue Considering the certain adjustment pressure after the A-shares rose in the early stage, the market's quantity and risk appetite will gradually decrease, and the short-term market is expected to continue to adjust. Technically speaking, although the channel of the index rise is still there, the MACD indicator of the Shanghai Composite Index is at a high level, and the green energy column is gradually expanding, indicating that the short-term adjustment has not yet ended. The Shanghai Composite Index may continue to test the short-term gap support in the short term. In the big direction, it is getting closer and closer to the time of the 19th National Congress. Referring to the overall trend of the market before and after the previous conferences, we predict that the risk of the index decline before the 19th National Congress is not large, and the market will generally maintain the pattern of high-level oscillations, and there will be no big ups and downs. If the index has a callback, it will be a better chance to increase the position. As for the futures index, the pattern of weak IH and strong IC is expected to continue. The IH short position can continue to be held in the short term. The first target is to see 2670 points and the second target is to see 2600 points. Guangxi Guiping Lidong Sports Goods Co., Ltd. , https://www.lidonggarment.com