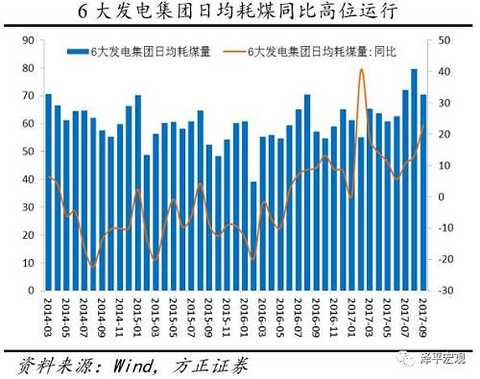

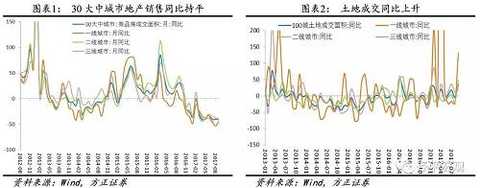

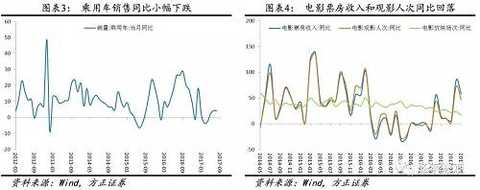

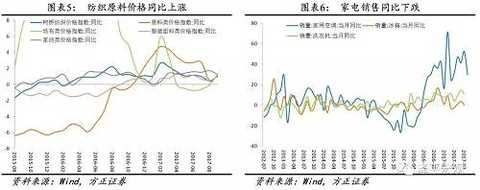

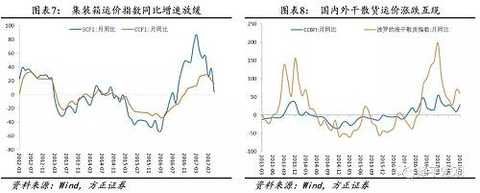

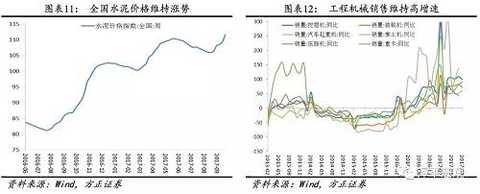

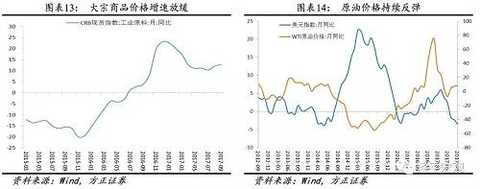

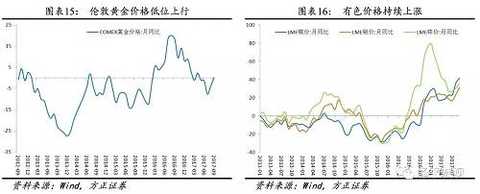

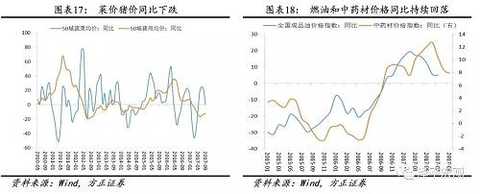

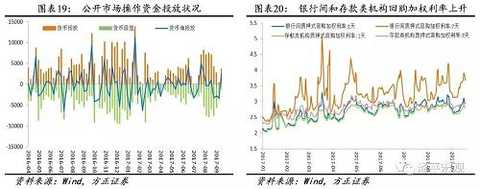

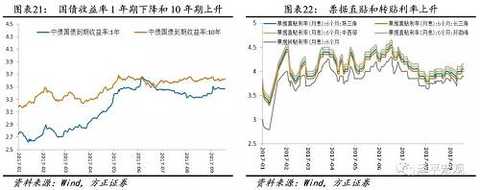

This article was first published on the WeChat public account: Zeping Macro. The content of the article belongs to the author's personal opinion and does not represent the position of Hexun.com. Investors should act accordingly, at their own risk. Text: Founder Macro Ren Zeping Contact: Gan Yuan Core point of view: In 2015, we proposed that “China’s economy may be close to the bottom and the future economy is L-shapedâ€. Since 2016, GDP growth has stopped falling, and quarterly GDP growth rate is very flat. 2016Q1-2017Q2 is 6.7%, 6.7%, 6.7%, respectively. 6.8%, 6.9%, 6.9%. Since the growth rate shift in 2010, the Chinese economy may be entering a new growth platform, with a wave of bottoming in 2016-2018. It is worth noting that in recent years, the micro-data is significantly better than the macro. For example, the GDP growth rate in the first half of 2017 was 6.9%, and the profit of industrial enterprises increased by 21% from January to July. After more than six years of market self-clearing, superimposed supply-side structural reforms in the past two years, the flat macro-capacity data such as GDP, industrial production, M2, and financial leverage have become more and more difficult to reflect the economic structural changes from the mid-micro world. For example, the de-construction of production capacity, the improvement of industry concentration, the remnant of the king, the strong and strong, etc., this significant difference between macro and micro is an important reason for the long and short differences in the market this year, which is roughly in line with our previous “new 5% ratioâ€. The old 8% is good" inference. In the fourth quarter of 2017 to the beginning of the year, the economic L-type, the demand side flat slightly decreased, the upward force comes from export recovery, real estate replenishment and land supply increase led to strong real estate investment, corporate earnings improved capital expenditure recovery, financing demand rebounded, etc. The downside factors come from the fiscal consolidation of infrastructure investment slowdown, restocking, and real estate-related declines. With the introduction of the destocking cycle after the fourth quarter, and the short-term measures such as production reduction and production restriction, environmental supervision and temporary suspension of work in the northern heating season, there will be some suppression on both sides of supply and demand, which may drag down economic growth. The short-term slowdown, but these temporarily suppressed production and demand orders will still be released at some point in the future, such as the end of the heating season in 2018. At the same time, the maintenance of the supply and demand gap is conducive to the continuous improvement of corporate profits, which will help to improve the valuation of these industries. The economic L-type has strong toughness and helps to improve the risk assessment factor of the DDM model. Under the support of fundamentals, since last year, A shares have gone out of a structural bull market dominated by consumption, cycle, finance, and real growth, if coupled with Tencent, Evergrande, Alibaba and other Chinese companies listed in Hong Kong and the US. Stocks, after the merger, the relatively comprehensive stock market representing the Chinese economy is a relatively bullish market. What needs to be considered in the future is whether it is possible to form a healthy slow-moving market by relying on performance recovery, strengthening supervision, and incorporating A-shares after reshaping such as MSCI? Can this value investment really take root in China and become a mainstream investment concept? Things are artificial. Downstream property sales are slower, land supply is accelerating, and car sales are better. The sales of 30-city real estate increased by 16.5% this week, compared with -40.9% in September, slightly lower than -40.6% in August. The first- and second-line land transactions in September increased sharply year-on-year. As of September 20, the first and second lines recorded respectively. 131.1%, 48.2%, much higher than August's -23.3%, -18.7%. Sales in the car market in September were good, although the year-on-year was low, but the chain increased by 14%. Retail and wholesale performed well; the composite index of textile raw materials rose year-on-year; the container freight index slowed down. In the middle reaches, the coal consumption of environmentally-friendly high-voltage power generation fell, and the steel price fell. Power consumption of power generation this week fell by 5.1% from the previous month, but as of September 21, the year-on-year ratio was 23.5%, which was much higher than the 13.2% year-on-year. The increase in coal consumption indicates that the company will accelerate its production in the future. The start of the blast furnace in the steel mill has been declining for five consecutive weeks, and the price of rebar fell by 1.1% on a week-on-week basis, but it was as high as 66.83%. Cement stocks fell for 7 consecutive weeks, and prices rose slightly overall. In August, the machinery market continued its hot momentum, and heavy trucks were “selling in the off-seasonâ€. The sales of excavators have maintained a 100% high growth rate for five consecutive months. Infrastructure promotion, renewal of demand, and low base are the main reasons for the popularity of machinery. The Fed announced that it will not raise interest rates temporarily, and the table will shrink in October. The US dollar has risen sharply and gold has dipped. The Iraqi Energy Minister announced that OPEC and other countries that have reduced production will consider extending or increasing production cuts to reduce global overcapacity, and international crude oil prices and non-ferrous prices continue to rise. Commodity prices fell, and the exchange rate of the RMB against the US dollar was low. Vegetable prices and meat prices in September both fell sharply year-on-year. This week's R007 interest rate was 3.8421%, up 38.71 BP from last week; DR007 interest rate was 2.9411%, up 3.12 BP from last week; 10-year bond yield was 3.6334%, up 3.84 BP from last week. This week, the renminbi depreciated sharply, hitting a new low since September 1, 17 years. Risk warning: Fed rate hike exceeded expectations; domestic currency tightening and financial deleverage exceeded expectations; real estate regulation is too tight; reform is lower than expected; debt risk. 1. Downstream: Real estate sales are low, and the first and second lines are accelerating, and the car sales are better. This week, 30 large and medium-sized cities real estate sales rose by 16.5%. As of September 20, real estate sales in 30 large and medium-sized cities were -40.9% year-on-year, slightly lower than -40.6% in August; among them, first- and third-tier cities were -44.7%, -39.2%, and -41.9%, respectively, higher than , below and below August, -53.2%, -37.5% and -37.7%. The land transaction area in September increased year-on-year. In September, the turnover of land in large and medium-sized cities was 35.0% year-on-year, much higher than the -4.9% year-on-year in August. The first-line growth rate rose to 131.3% from -23.3% in August; the second-line rose from -18.7% in August to 48.2. %; the third-line rose from 18.1% in August to 18.8%. The increase in land sales was mainly due to the acceleration of land acquisition in first- and second-tier cities. In September, the land supply of large and medium-sized cities increased by 38.8% year-on-year, down from 45.5% in August. The year-on-year growth rates of land supply in first- and third-tier cities were 178.7%, 21.9% and 40.9%, respectively, which were lower than August's 238.7%. 26.6% and 55.0%. The car market in September was generally better. In terms of retail sales, the retail sales volume of the auto market in September this year was about -3.3%, but mainly due to the high base of 49% in September last year: 14% in September is still higher, indicating that the retail market is better. In terms of wholesale, this week's sales of manufacturers increased by 2.5% year-on-year, and the performance was equally good. Last week, the release of new films boosted the box office revenue by 5.5%, and the number of people watching and screening was 5.6% and -3.8% respectively. Compared with the same period of last year, box office receipts, movie attendances and screenings in September were 57.5%, 46.3% and 17.1%, respectively, which were lower than 85.0%, 72.8% and 23.1% in August. The price of textile raw materials rose year-on-year. As of September 20, the raw materials, grey cloths, apparel fabrics and home textiles of Keqiao Textile Price Index increased by 1.16%, 1.24%, 0.96% and 1.24% respectively, up 0.71% and 1.25% respectively from the previous month. , up 0.49%, down 0.49%. Container freight rates have slowed down. Last week, the Shanghai Export Container Freight Index (SCFI) rose by 0.04% from the previous month to 3.7% in September, down from 37.8% in August. China's Export Container Freight Index (CCFI) closed down by 1.18% last week, compared with 16.0% in September, down from 21.3% in August. This week, the Baltic Dry Index (BDI) fell 8.6% month-on-month, compared with 58.5% in September, down from 69.8% in August. Last week, China's coastal dry bulk freight index (CCBFI) fell 0.1% from the previous month, compared with 28.4% in September, up from 9.5% in August. 2, the middle reaches: environmental protection, high-voltage power consumption, coal consumption fell, the steel price fell, the cement rose, the machinery was hot Power consumption of power generation this week fell. The average daily coal consumption of the 6 major power generation groups decreased by 5.1% from the previous month. As of September 21, the average daily coal consumption of the six major power generations was 704,000 tons, down from 797,000 tons in August. Coal consumption in September increased by 23.5% year-on-year, higher than August's 13.2% and July's 10.6%. The increase in coal consumption for power generation indicates that the company will accelerate its production in the future. Domestic steel mills' profit ratio last week was 85.3%, down 0.6 percentage points from the previous week and still remained at a high level. Last week, the national blast furnace operating rate was 75.8%, down 0.2 percentage points from the previous month. Subject to the policy pressure, the operating rate has been declining for five consecutive weeks. August crude steel output was 8.7% year-on-year, down from 10.3% in July but up to 5.7% in June. As of September 20, rebar prices fell by 1.1% on a week-on-week basis, up 66.83% year-on-year, up from 61.32% in August. In the future, it is expected that high-pressure production and peak season will continue to support steel prices to remain high. Cement prices have risen slightly and corporate inventories have continued to fall. Cement prices rose 0.96% month-on-week this week, up 25.3% year-on-year in September, down from 27.4% in August. Last week, the national cement storage capacity fell by 2.63% from the previous month to 62.5%, which has been falling for seven consecutive weeks. In August, weak demand was superimposed on environmental supervision, and cement production fell sharply. Commodity prices have risen and fallen. As of September 20, there were 58 kinds of commodities with rising commodity prices in the list of rising and falling prices, concentrated in the chemical sector (29 kinds) and colored plates (8 types in total). The top 3 products were formaldehyde (37%). (6.94%), fatty alcohol (4.94%), sulfur (granules) (3.34%). There were 37 kinds of commodities with a decrease in the chain ratio, which were concentrated in steel (13 kinds in total) and rubber (9 kinds in total). The top 3 commodities were egg (-2.65%), LDPE (-1.52%) and hot rolled coil (- 1.18%). The machinery market continues its hot momentum. In August, heavy trucks continued the "off-season hot sale" situation: Since March this year, the national heavy truck sales have exceeded 90,000 vehicles for six consecutive months, of which the top ten heavy truck companies in August sales reached 83%. According to the statistics of China Construction Machinery Industry Association, the sales volume of major domestic excavator manufacturers in August has exceeded 1 year-on-year, and has maintained a super high growth rate of more than 100% for five consecutive months. Overall, infrastructure promotion, newer demand, and low base are the main reasons for the popularity of machinery sales data this year. 3, upstream: the Federal Reserve shrinks gold diving, oil prices continue to rise This week, the CRB industrial raw materials index was 0.5% from the previous month, and 12.7% from September, up from 12.0% in August. The South China Industrial Products Index increased by -3.4% from September, compared with 44.3% in September, up from 41.4% in August; South China Agricultural Products was 0.00061, and the stock index was -0.5%, compared with 2.4% in September, unchanged from August. The Federal Reserve announced on September the statement of the September meeting on interest rates, decided to maintain the federal funds rate range of 1-1.25% unchanged, will start to reduce the balance sheet from October, 10 billion US dollars per month, and is expected to raise interest rates once this year, next year Raise the interest rate three times. After the announcement, the US stock market fell first and then rose, the US bond yield rose, and the US dollar rose. This week, the US dollar index rose by 0.7% month-on-month, compared with -3.5% in September, down from -2.3% in August. Affected by the Fed’s “reduction†and expected interest rate hike at the end of the year, gold plunged and the price of gold fell back below $1,300 per ounce. Due to the small scale and high certainty in the initial stage of “shrinking the tableâ€, it is in line with market expectations. According to the interest rate expectation dot map, it is expected that there will still be a rate hike at the end of 2017, and the interest rate hike will be applied at the end of the year. After the Iraqi Energy Minister announced that OPEC and other countries that have reduced production will consider extending or increasing production cuts to reduce global overcapacity, international oil prices have risen, creating the third-quarter maximum gain in 13 years. This week, Brent crude oil prices rose by 1.2% month-on-month, compared with 15.2% in September, up from 10.0% in August. If OPEC complies with the agreement to reduce production, the macro market background of the oil market will improve, oil demand may be stimulated to grow, and oil prices will continue to rise. During the week of September 15, EIA crude oil inventories increased by 4.591 million barrels, which recorded growth for three consecutive weeks. It is expected to increase by 3.493 million barrels, which exceeded market expectations. Refined oil inventories decreased by 5.693 million barrels, the week of November 11, 2011. Since the new low; gasoline inventories decreased by 2.125 million barrels, recorded a decline for three consecutive weeks, the market is estimated to reduce 2.025 million barrels. Non-ferrous prices continued to rise, and copper, aluminum and zinc prices continued their upward trend. LME copper was 1.0% MoM this week, compared with 41.5% in September, up from 36.1% in August. LME aluminum prices fell 4.6% on a week-on-week basis, compared with 31.4% in September, up from 23.7% in August. LME zinc prices increased by 4.2% on a week-on-week basis, compared with 35.4% in September, up from 30.6% in August. 4. Price: prices of vegetables, pork, refined oil and medicinal materials are falling. With the end of the exchange period and the better weather in Shandong, the average wholesale price of 28 key monitored vegetables in the Ministry of Agriculture decreased by 22.37%, the wholesale price index of Qianhai vegetables decreased by 21.46%, and the wholesale price index of vegetables in Shandong decreased by 44.66. %. The average wholesale price of 28 key vegetables monitored by the Ministry of Agriculture, the Qianhai Vegetable Wholesale Price Index and the vegetable wholesale price index of Shandong Province were -31.0%, -33.7% and -36.6%, respectively, all lower than the 4.54% in August. 1.0% and 13.8%. The average wholesale price of pork in the Ministry of Agriculture dropped 19.5% this week, compared with -40.9% in September, down from -19.6% in August. The average retail price of pork in 36 cities fell by 59.9% from the previous month and fell by 43.6% year-on-year in September. The average retail price of beef and mutton in 36 cities was -37.8% and -38.9%, respectively, in September, which was lower than -0.2% and -2.4% in August. The average retail price of grass carp and carp in 36 cities was -33.1% and -32.5%, respectively, in September, which was lower than 9.5% and 19.7% in August. In terms of non-food, oil and drug prices continued to fall year on year. The national refined oil price index fell by 88.3% year-on-year in July. On September 1, the National Development and Reform Commission announced that the price of refined oil products in the country will not be adjusted. The unadjusted amount will be added or offset when it is included in the next price adjustment. China's Chengdu Chinese herbal medicines price index fell 19.1% year-on-year in September. 5. Currency: The central bank maintains “cutting the peaks and filling the valleyâ€, and the RMB exchange rate against the US dollar is low. This week, the central bank's open market has a total of 90 billion reverse repurchase due, Monday and Tuesday no reversal repurchase due, 30 to 60 billion and 30 billion from Wednesday to Thursday, and MLF expires 113.5 billion on Monday, no repurchase and central this week. The ticket expires. From last Thursday to this Tuesday, the central bank achieved a net launch for 4 consecutive days, with reverse repurchase amounts of 100 billion, 200 billion, 300 billion and 150 billion. On Thursday and Friday, there were zero returns for two consecutive days. From the point of view of market liquidity, the central bank will continue to maintain the operation strategy of “shaving the peaks and filling the valley†in September, and continue to implement large-scale net investment, indicating the attitude of calming the seasonal fluctuation of liquidity, but the funds are still overall this week. Tight, the main push is still the corporate tax payment. As of September 20, the 1-day inter-bank repo plus rights ratio was 2.9818%, up 25.89 BP from last week; the 7-day inter-bank repurchase plus rights ratio was 3.8421%, up 38.71 BP from last week. As of September 21, the 1-day deposit-type institutions repurchased plus rights ratio was 2.8269%, up 13.44 BP from last week; the 7-day deposit-type institutions repurchased plus rights ratio was 2.9421%, up 3.12 BP from last week. As of September 21, the 1-year bond yield was 3.4715%, down 0.85 BP from last week; the 10-year bond yield was 3.6334%, up 3.84 BP from last week. As of September 21, the Pearl River Delta bill direct interest rate (monthly interest rate), the Yangtze River Delta bill direct interest rate (monthly interest rate) and the bill transfer rate (monthly interest rate) increased by 5.0 BP from last week. This week, the credit spreads of different maturities narrowed and partially relaxed. The credit spread of 1-year AAA corporate bonds eased by 1.45 BP, and the credit spread of 10-year AAA corporate bonds narrowed by 0.9 BP. As of September 21, the RMB exchange rate has depreciated sharply, and the long-term depreciation pressure has decreased. This week, the central parity of the yuan against the US dollar depreciated 4.02%, the lowest since September 1, 2017. The spot exchange rate of the RMB depreciated by 3.91%. As of September 20, the offshore RMB depreciated by 3.87 percent. As of September 20, the onshore and offshore RMB exchange rate spreads narrowed from 0.0168 last week to 0.0122, and both onshore and offshore RMB against the US dollar fell below the 6.60 mark. The US dollar against the RMB 1-year foreign exchange forward purchase price fell 160.00 BP. Dye Fabric,African Batik Fabric,African Brocade Fabric,Dye Colored Fabric changxing weituo import and export co.,ltd , https://www.cxweituo.com